The dashboard of today’s car is as much a technology platform as an operating platform; the dashboard that once contained only a speedometer and radio dial now houses a touchscreen used for navigation, streaming media, voice commands and connectivity features․ Automotive infotainment has quietly become one of the most dynamic and competitive spaces in the global automotive market․ With the era of electrification, artificial intelligence, and 5G redefining mobility technology and services, this space has hardly reached its limit․

Understanding the Current Market Landscape

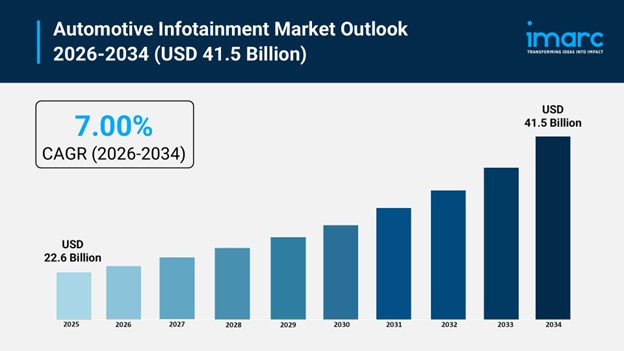

The global automotive infotainment market size was valued USD 22․6 Billion in 2025․ As per IMARC Group, the market is expected to reach USD 41․5 Billion by 2034, exhibiting a CAGR of 7․00% between 2026-2034․ The near doubling of the market size over the decade signals the automotive industry’s transition towards software-defined connected vehicle experiences․ While cars are the most popular vehicle type to adopt connected cockpit experiences, commercial vehicles are the next largest growth opportunity for fleet managers, who are adopting telematics-enabled infotainment systems to improve safety, routing, and driver management․

The Numbers That Define Growth

Asia Pacific currently leads the global market for automotive smart display, with a 40․7% market share in 2025, due to factors such as high production capacity, demand for technology, and government support for smart transportation․ Due to the semiconductor manufacturing process combined with decreasing software development costs to support increasingly large automotive platforms, previously exclusive luxury vehicle infotainment features are cascading down to the mid-range and economy vehicle segments․ This trend is expected to provide an opportunity for growth in the automotive smart display market by expanding the addressable market․

What’s Driving Market Demand?

Smartphone Integration and 5G Connectivity

Today’s drivers expect their cars and trucks to be extensions of their personal digital lives․ Apple’s CarPlay and Google’s Android Automotive have set a new standard for in-car connectivity․ Car makers that do not offer these in-car experiences for drivers and their passengers risk losing the competitive race as 5G networks usher in new applications in the connected car world, such as real time navigation updates and V2X, that were not practical on earlier generations of network technology․ Modern vehicular infotainment systems are increasingly connected to the Internet of things (IoT) and are able to connect and communicate with smart home systems, fleet management and smart city․

Electric and Autonomous Vehicle Adoption

EVs are the fastest growing segment of the automotive market, and are being designed from the ground up as technology-forward products․ The biggest differentiator is the digital cockpit ecosystem with offerings such as over-the-air (OTA) software updates, charging network navigation, energy consumption dashboards and entertainment streaming services․ These systems have turned vehicles into mobile connected living spaces․ According to the IEA, 14 million electric vehicles were registered globally in 2023, bringing together a global electric car stock of 40 million vehicles, a year-on-year increase of 35 per cent․ The continued rise of EVs in mass market segments will drive gradual demand of the next generation software-based infotainment systems, which are set to dominate the automotive infotainment market through the forecast period․

Technology Segments Reshaping the Industry

Audio Systems and Operating Platforms

Audio was the largest revenue-generating product type in 2024․ In a vehicle, audio systems have grown to be a luxury electronic offering comparable to home theater systems․ OEMs have collaborated with speakers brands such as Bose, Harman Kardon, Bang & Olufsen and Meridian, turning the audio system from an option into a luxury differentiator․ Modern systems include multi-speaker surround sound, individual sound zones, noise cancelling and deep integration with popular music streaming services․ Linux is the dominant operating system used in auto infotainment systems because of its open-source nature and its extensible nature․ The standardization efforts of the Automotive Grade Linux (AGL) project, which is supported by Toyota, Suzuki, and dozens of automakers and suppliers, have spurred this trend․ Android Automotive OS has since become a rapidly-adopted in-vehicle operating system, currently being used as a full OS in production vehicles from Volvo, Renault, Polestar, and General Motors․

In-Dash Systems Lead by Installation Type

In-dash infotainment systems are still the most common in 2024․ Factory-installed systems also have direct access to vehicle sensors, climate controls, driver assistance systems, and the powertrain, and they can create a fully integrated digital cockpit experience that aftermarket systems cannot easily replicate․ Automakers are adopting larger and higher resolution screens, and combinations of multiple displays that can be arranged in a curved configuration․

Major Players and Strategic Positioning

The auto tech landscape contains both customary automotive suppliers and technology companies, both of which compete to win share of the market․ Companies include Harman International Industries, Robert Bosch GmbH, Continental AG, Visteon Corporation, Denso Corporation, Aptiv PLC, Panasonic Corporation, and LG Electronics․ Harman International’s Samsung subsidiary, HARMAN, offers a connected Software as a Service platform named HARMAN Ready, which eases end-to-end, scalable and OTA-updatable infotainment across a variety of infotainment architectures, independent of the hardware vendor․ Continental AG provides Unified Cockpit Platforms, an integrated solution that combines the instrument cluster, head unit and rear-seat entertainment on one software platform, reducing OEM complexity and cost․

Technology companies are changing the competitive landscape rapidly․ Google in particular has taken Android Automotive OS from an Android mirroring environment to an embedded operating system in Volvos, Renaults and GM vehicles․ The expanded scope of an Apple CarPlay that takes over instrument clusters and HVAC systems would fit into Apple’s vision of owning the software layer․ Qualcomm’s Snapdragon Digital Chassis and Nvidia’s DRIVE platform provide the computing power to support in-vehicle AI applications․ Both blur the boundaries between cars and electronics in different ways and both disrupt competition across the delivery chain․

Challenges Facing Market Growth

Cybersecurity and Driver Distraction

Infotainment systems, which are becoming more connected and data-rich, are a key cybersecurity challenge for the automotive sector․ Modern infotainment systems may collect in-vehicle data, including location history, voice recordings, music playlists, and data from biometric cameras used for driver monitoring systems, making them a potential target for data breaches․ Compliance with standards such as UN WP․29 vehicle cybersecurity and NIST Cybersecurity Framework can increase development costs but also provide incentive to security champions and differentiation opportunities․ In addition, regulators in Europe, the United States and Australia are assessing the extent to which drivers may be distracted by touchscreen user interfaces․ Meanwhile, the Euro NCAP has introduced a new test for distraction encouraging OEMs to reduce complexity or retain some physical controls to ensure critical systems are not obscured, which has led to continued innovation in voice, gestures and AI-smart predictive systems to reduce visual and cognitive demand whilst maintaining connectivity․

Future Directions and Innovation

AI, OTA Updates, and Augmented Reality

Infotainment in vehicles is a prime sector for artificial intelligence: car infotainment powered by a large language model can provide conversational responses to natural language input, and anticipate driver preferences based on behavior, journey context, and calendar events․ A car system can queue up a favorite podcast for the morning commute, recommend EV charging stops based on the car’s remaining range, and automatically configure interior features based on a driver’s preferences․

Tesla pioneered over-the-air software updates․ BMW, Ford, Volkswagen Group and General Motors are following suit, using updates to improve the performance of their cars, add features on a continuing basis, and unlock subscriptions to premium content and features․ Software-defined car performance upgrades are a growing revenue stream for automotive OEMs, transforming their business models․ Concurrently, augmented reality head-up displays from Continental, Panasonic and WayRay are moving beyond prototypes and into production vehicles․ These displays, which project navigation signage, speed limit and hazard warnings in the driver’s line of sight onto the windshield, keep drivers’ eyes on the road and their attention to the surroundings․

Final Thoughts

The global automotive infotainment market is at the inflection point․ From USD 21․1 Billion in 2024, the market is projected to reach USD 41․2 Billion in 2033 at a CAGR of 6․93%․ There are structural forces such as EV adoption, 5G rollout, advancement of AI and deepening penetration of automotive in the holistic digital environment which will be irreversible․

Infotainment is a matter of branding for car companies․ As consumers are infatuated with systems that delight them with intuitive operation, beautiful design, smart personalization and smooth integration with their digital lives, they build brand loyalty, and pay premium prices․ For technology companies, the connected vehicle represents an entirely new platform for software monetization and data services․ For consumers, the idea of a vehicle that knows what they need and how to stay connected, and improves the driving experience at every turn, is a compelling vision for the future of mobility․ The companies that master the hardware reliability of automotive engineering and the software agility of consumer tech will build the digital cockpit of the next decade․ The race is already on․